All eyes will be on TD’s U.S. results and strategy when it kicks off bank earnings season on Thursday

Author of the article:

Bloomberg News

Christine Dobby

Published Aug 21, 2024 • Last updated 6 hours ago • 5 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

A Toronto-Dominion (TD) bank branch in Toronto on March 15, 2023. Photo by Cole Burston/Bloomberg

Article content

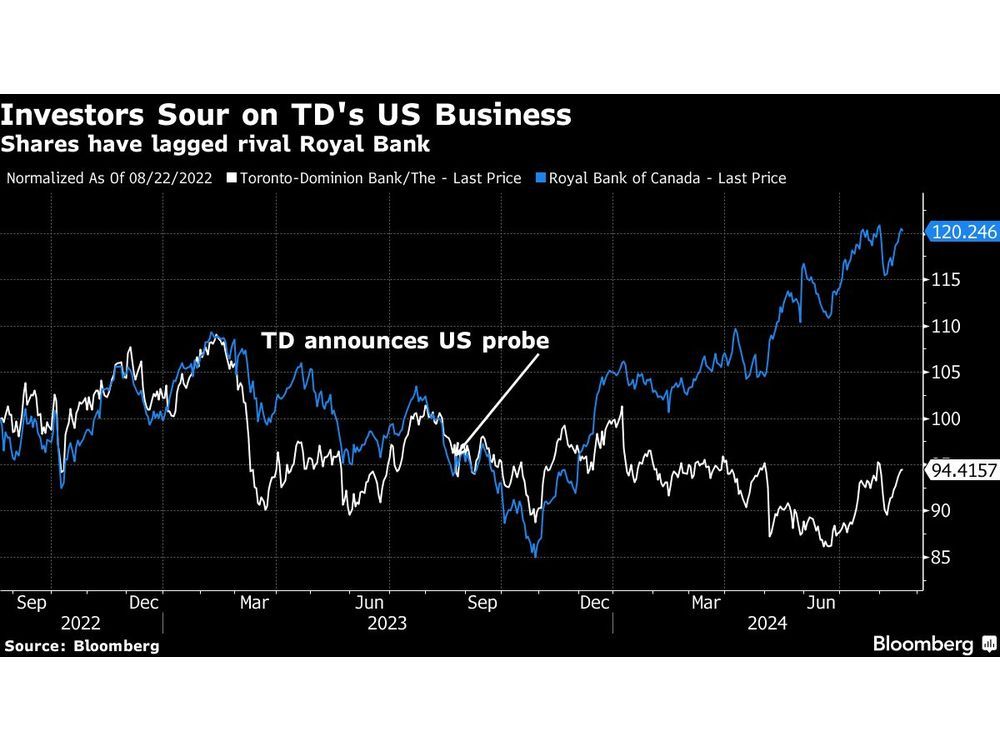

Toronto-Dominion Bank’s expensive foray into the U.S. was supposed to supercharge its growth. Instead, it’s become a drag on profitability and badly dented the lender’s reputation.

A busted US$13.4 billion takeover of First Horizon Corp., a money-laundering probe into its U.S. branches and anemic returns across its stateside operation have investors turning sour on Canada’s second-largest bank. Despite some positive momentum in recent weeks, its stock has way underperformed all other major Canadian banks.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Those once-prized U.S. assets, which include more than 10 million customers, accounted for about 23 per cent of net income and 25 per cent of revenue in the most recent quarter. Those operations used to deliver a nice valuation premium for the stock. Now, some investors believe they aren’t delivering on their promise.

“The U.S. is a tougher market to operate in. It’s not as profitable, it’s more competitive. And the relationship with the regulator is less friendly,” Brian Madden, chief investment officer at Toronto-based First Avenue Investment Counsel Inc., said in an interview. While he applauded Toronto-Dominion’s attempt to seek U.S. growth, he now counts his firm as a “frustrated shareholder.”

All eyes will be on Toronto-Dominion’s U.S. results and strategy when it kicks off Canadian bank earnings season on Thursday. The lender faces the threat of billions of dollars in fines and — maybe worse — the prospect that regulators will impose limits on future U.S. growth. A spokesperson declined to comment, citing a quiet period ahead of its earnings release.

Posthaste

Breaking business news, incisive views, must-reads and market signals. Weekdays by 9 a.m.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Posthaste will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“Once again, TD heads into reporting season in a unique position as anti-money laundering issues at the bank overshadow quarterly results,” Scotiabank analyst Meny Grauman wrote in a report to clients this week.

Grauman said he sees TD as a value opportunity, considering “the market is now ascribing negative value to its U.S. business.” Investors seem to have a one-way view: signs of weakness are “likely to be severely punished,” while strong results aren’t likely to cause a rally in the share prices because investors are still waiting for a resolution to the AML problem.

TD executives have said they remain confident in the U.S. business, notwithstanding the U.S. regulatory woes. Chief executive Bharat Masrani told investors last year the division still has “substantial growth potential — there are three times as many customers in our U.S. footprint as there are in all of Canada.”

‘Go big or stay home’

Toronto-Dominion has struck deals worth just over US$25 billion in the U.S. over 20 years, according to data compiled by Bloomberg, thanks to an acquisition spree kickstarted by former CEO Ed Clark.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

While Canada has one of the most stable and profitable banking sectors in the world, it’s almost completely carved up by its six largest lenders, leaving them fighting over scraps of market share.

“You need to go big or stay home,” Clark told Bloomberg in 2011, after Toronto-Dominion spent about US$6.3 billion to acquire auto lender Chrysler Financial. “You don’t want to be stuck in this mid-sized space.”

That deal was one of four major stateside acquisitions announced since 2004. Others included the US$8.5 billion takeover of New Jersey’s Commerce Bancorp in 2008; a roughly US$7 billion purchase of Banknorth Group, which was completed in two steps by 2007; and the US$1.3 billion acquisition of brokerage Cowen Inc., which closed in 2023.

The deals have made Toronto-Dominion’s U.S. holding company the 10th largest bank in the country by assets as of the end of March, according to regulatory data. With a network of almost 1,200 branches stretching from Maine to Florida, it has more retail locations in the U.S. than in Canada.

Then came its pact in 2022 to buy First Horizon, a regional player in the southeastern U.S., in what would have been its largest-ever deal. The parties walked away in May 2023, saying it was unclear regulators would ever greenlight the deal.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The collapse was a blow to the credibility of Masrani, who led the U.S. business during Clark’s expansionary days.

Soon after, Toronto-Dominion had to acknowledge that it was receiving inquiries from the U.S. Department of Justice, in addition to financial regulators and the Treasury Department. The core allegations are that it failed to catch money laundering and other financial crimes at several U.S. branches. Analysts have speculated that penalties may run into the billions and that the bank may face curbs on its business — similar to how Wells Fargo & Co. was punished in a fake accounts scandal.

In the fallout, TD has replaced about 10 senior leaders in compliance and legal roles — and fired about a dozen customer-facing employees — and has already spent $500 million to bulk up its anti-money-laundering defences.

‘Subsidized’ returns

As ugly as that is, some investors find something else even more problematic at Toronto-Dominion: it just doesn’t earn attractive returns in the U.S.

Nigel D’Souza, senior investment analyst at Veritas Investment Research, estimates the U.S. retail bank’s return on equity was just 8.5 per cent in fiscal 2023, according to his analysis. That compared with a 36.8 per cent return in its Canadian personal and commercial banking business. Return on equity is a critically important metric of bank profitability, measuring how much shareholders get for each dollar of equity capital.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Toronto-Dominion’s disclosures make the U.S. business seem rosier, D’Souza said, because “they have returns that are subsidized,” with some treasury and corporate expenses allocated to the bank’s general corporate segment — including significant investments in strengthening risk controls.

“The major U.S. banks generate higher profit margins and most outperform TD,” D’Souza said. “My argument to my clients is if you want exposure to U.S. banking, just buy a well-run U.S. bank instead.”

There are signs investors are doing just that. Toronto-Dominion shares have fallen 3.6 per cent over the past 12 months; its five biggest rivals have gained an average of 17 per cent.

That underperformance, coupled with negative headlines on the money-laundering probes, have also put a target on the back of Masrani, who has been CEO for almost 10 years.

“Having a different leader could change sentiment around the stock,” D’Souza said. “But it is not going to improve the ROE of the U.S. banking franchise. It’s not going to make the industry any less competitive.”