Falling interest rates to bring flood of funds back to financials, REITs, utilities and telecoms

Published Sep 05, 2024 • Last updated 7 hours ago • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

The tide is turning for dividend-paying Canadian stocks and financials are likely to be the biggest winners, says CIBC. Photo by Peter J. Thompson/National Post

The quick rise in interest rates over the past few years drove many investors into term deposits and other short-term fixed income products. CIBC estimates over $200 billion went to these products that normally might have bought high-yielding equities.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

“With falling rates, it makes intuitive sense that some of this will reverse – but also reasonable to ask “when” will this occur?,” said CIBC analysts led by Ian de Verteuil in a research note.

To answer that question the CIBC team looked back at funds flow of Canadian bank term deposits over the past 35 years. There have been four periods of “meaningful” term-deposit outflows and on average they occurred 350-400 days after the peak in the 3-month bill and 2-year bond rates in Canada.

“Interestingly, these two rates actually peaked in October 2023 and have been falling since,” they said.

So where will the money go?

CIBC believes high-dividend-paying Canadian stocks are a “natural” home for these funds as they offer tax advantages over interest income and dividends can grow over time. The relative yield of these stocks compared with 2-year government rates is also becoming increasingly attractive, they said.

“Sectors such as REITs, Utilities, Telecoms and Financials have added appeal of better-than-average business and earnings stability,” said the analysts.

Posthaste

Breaking business news, incisive views, must-reads and market signals. Weekdays by 9 a.m.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Posthaste will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

CIBC expects the Bank of Canada‘s overnight target rate to fall to 3.75 per cent by the end of this year and 2.5 per cent by the end of 2025.

If its forecast bears out, the decline in rates at this pace should drive investors back to Canadian dividend paying stocks, especially since many of these equities have performed poorly compared to the boarder market over the past few years.

“If interest rates fall as we expect, what was a material headwind should turn by 180 degrees and provide support for REITs, Utilities, Telecoms and Financials. We expect these sectors to outperform in the coming quarters,” said the analysts.

But money flow is not enough; business performance also matters.

Telecoms face the challenges of more competition and changing regulations and some Real Estate Investment Trusts are still suffering from the impact of the COVID-19 pandemic and hybrid work, said the analysts. Utilities have to contend with a shift in power generation.

“Financials are likely to be the biggest winners,” said de Verteuil’s team.

Bank earnings out last week show the strength of the domestic personal and commercial banking business, and life insurers are managing the changing rate environment.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

“As such, we expect most flow into these traditional outperformers,” the analysts said.

Sign up here to get Posthaste delivered straight to your inbox.

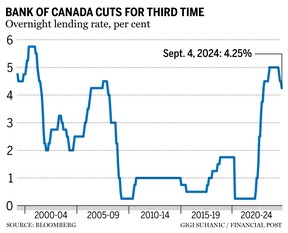

The 25-basis-point cut was widely expected but some still thought the central bank should have gone further.

“It’s said that victory goes to the bold, but the Bank of Canada went with the more cautious approach of yet another quarter point rate cut,” said Avery Shenfeld, chief economist at CIBC Capital Markets, after the decision.

“That left rates still well above where they will have to head to get the economy and labour markets into better shape.”

Something to know — aside from the pandemic, the last time the central bank cut its rate three times in a row was in 2009 at the height of the global financial crisis.

John McKenzie, CEO of TMX Group, will speak at the 2024 Scotiabank Financials Summit in Toronto

Today’s Data: Canada labour productivity, United States non-farm productivity, ADP employment change

Earnings: Enghouse Systems Ltd., Broadcom Inc.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Gold investors returning from their summer holidays will be eager to see whether the precious metal can sustain its record-breaking rally or if it will succumb to the curse of September.

Bullion has dropped every September since 2017. Over that period, the average decline has been 3.2 per cent in September, easily the worst month of the year.

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line with your contact info and the gist of your problem and we’ll try to find some experts to help you out, while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers, led by Julie Cazzin, can give it a shot.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Plus check his mortgage rate page for Canada’s lowest national mortgage rates, updated daily.

Today’s Posthaste was written by Pamela Heaven, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.